I have equity in some pawn shops, payday loan, title loan, personal loan… brick-n-mortar locations. I belong to a couple of industry groups & associations in a multitude of States.

The following is what ONE entrepreneur has chosen to do to remain open. I am not endorsing it. Rather, sharing it with you. This is actually provided by Yigal’s Group for pawnshop owners. [Consultant/Coaching for Pawnshops]

Think!

We SINCERELY hope you and your Team are doing well.

It’s tough around the globe BUT I’m very optimistic about the eventual outcome of our industry!

I want to EMPHASIZE that WE – those of us in the business of lending to the masses – are about to experience the most profound changes and OPPORTUNITIES imaginable!

Face-to-face interactions will diminish PERMANENTLY. Digital behaviors and transactions ordinary people can execute from their phone will scale significantly. Embrace a digital experience theme for your life, your brand, your business, for YOU, or “die!”

Disruption = Opportunity!!

Demand by consumers for solutions for their financial challenges is going to scale beyond our resources! If you need help adapting to this new paradigm, REACH OUT. If I cannot help you, I KNOW who can!Jer TrihouseConsulting@gmail.com

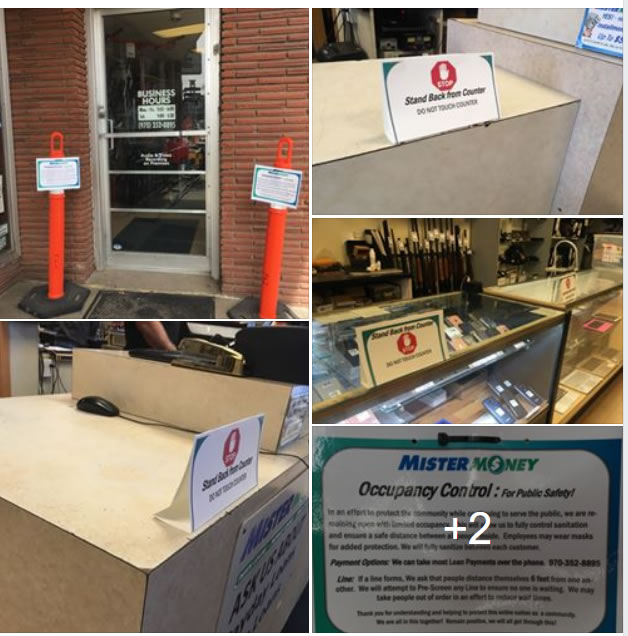

Steven A: What’s working for us:

We want to limit the people for moral reasons and stay open to serve those in need and to survive as a business.

I am feeling good that our plan is working; we are serving and we are not creating a “Spreading” scenario.

We have Signs in front of the Door Stating Limited Capacity (As Pictured).

We have an cheerful happy friendly employee at door who watches, counts and allows in and out.

If line is too crowded outside, employee tells them to spread out.

Door employee talks to the line while waiting and asks what they are up to, pre screens… rewrites can go in and out quick, loans on crazy stuff may get told “not today”. Answers questions, makes sure no one is waiting for no reason. Also makes sure no one is sick coming in. This is not as hard as it sounds. No one has any issues with it.

Employee opens and closes door no one else touches door handle.

We have four stations. We are low on employees, but basically allowing one customer per employee / station.

Station is wiped down between customers.

Station / Counter has a Triangle sing on it preventing people from leaning on counter. Without this barrier they will lean, you need the triangles (as pictured). This keeps them standing upright which keeps them 5-6 feet away, a rope barrier would work as well. But you need a barrier otherwise they will come and get a foot from your face just out of habit.

Pens. We have a Clean Pen and Dirty Pen jar. Instruct them to take a clean pen, and put in dirty pen jar when done. Watch them because they will put it right back in the clean.

Money and ID and such just goes on counter, no need to handle it.

We also tell the customers “Remember, the money is likely dirty, be careful with it, and use the hand sanitize anytime you handle money”.

Send em on the way.

Employees can wear masks if they want but none are, as long as customers are keeping distance they feel good.

Yes, we speak up if someone is breaking the new social mores, wandering around pointlessly, getting too close, any cough we ask to leave.

When we control the door people understand we are serious and it gives us the chance to tell them its really important and hopefully if we all follow the safe practices it will be a short lived thing.

People are buying quick and easy. Game systems, firearms, TV’s. Quick easy, not even asking for discounts. Just go grab a TV and Checkout, kinda nice.

We had the system down to a tee yesterday and I believe we kept everyone 6 Feet away from one another.

Think we did our social responsibility and that we were NOT a place where infection is being spread.

We also got money to those in need and made a bit of money ourselves, (Not much but a little at least).

Hope this helps. We are in a city of 120,000 BTW. Not high density. Mostly suburban.

This is for our Texas lenders. It was issued 20 minutes ago.

It’s likely to serve as a template for the majority of States so I suggest you take a look.

Meanwhile, prepare to SCALE if you’re so inclined!

You may visit the OCCC link to read their PDF.

From: rule.comments@occc.texas.gov

Date: Tue, Mar 17, 2020 at 2:48 PM

Subject: OCCC Advisory Bulletin on Coronavirus Emergency Measures for Credit Access Businesses

To: Jer XXXXX

Don’t Allow the Government to Dictate Consumer Lending: <36% APR Coming

Thanks for being a loyal reader. I appreciate hearing from you. Let me know if you ever have any questions, ideas, or comments… Jer@TheBusinessOfLending.com

As Nobel prize-winning economist Paul Samuelson famously testified in 1969:

“The concern for the consumer and for the less affluent is well taken. But often, it has been expressed in a form that has done the consumer more harm than good.”

“For fifty years, the Russell Sage Foundation and others have demonstrated that setting too low ceilings on small loan interest rates will dry up legitimate funds to the poor who need it most and send them into the hands of the illegal loan sharks.”

“History is replete with cases where loan sharks have lobbied in legislatures for unrealistic minimum rates, knowing that such meaningless ceilings would permit them to charge much higher rates.”

It’s already happened in several States!

Read the original & full text at American Commitment.Org

REJECT A GOVERNMENT TAKEOVER OF CONSUMER LENDING By Phil Kerpen

NOTE: We are consultants for entrepreneurs who want to start or improve their payday loan business operations. We are not Lenders. We teach, consult, offer Courses and provide boot camps and phone consulting services enabling entrepreneurs with a desire to enter this industry to avoid failure. We opened our first location in 1998 in Garden Groove, Calif. Today we own stores and online lending portfolios. Additionally, we teach, lecture, speak, consult entrepreneurs and companies in “The Business of Lending to the Masses.”

For more information about our services, visit: Start Here

The following is a VERY BRIEF overview extracted from our 500+ page Course: “How to Lend Money to the Masses Profitably.”

Are you interested in starting a payday loan company in Canada? In one province? Online?

First Question: What is a payday loan

In Canada, a payday loan is a short-term loan with high fees for solving immediate, short-term financial emergencies.

Payday loans are “expensive” money. Generally, depending on the Canadian Province, a payday loan consumer may borrow up to $1,500.

Borrowers must pay the loan back from their next paycheque. Failure to pay back these loans on the promised due date result in more fees and interest charges.

This will likely increase your loan principal.

Payday loans are designed to solve a cash shortfall until your next pay. Avoid using them for ongoing costs such as rent, groceries or utility bills. If you use them in this way, you may end up in financial trouble.

Both private and publicly traded companies offer payday loans in stores [brick-n-mortars] and online.

What to expect when you start a payday loan business

Here’s what you can expect if you’re considering opening a payday loan company.

The easiest method to determine the legalities involved is to simply get a payday loan. Visit your nearest competitor in your city and go through the process.

Get copies of everything; all the forms.

Look around! Whip out your phone and take pictures of any wall charts, regulatory info, consumer help alerts posted inside the location…

If there are payday loan stores around you, you know they’re legal!

So… get a payday loan/installment loan/title loan… Then, pay back the money in a couple of days. Consider this your first “investment” in your new business.

PS: If you cannot qualify for a loan at your competitor’s store, get a “shill.” Pay their fees.

Our Course covers EVERYTHING you need to know about starting and operating a payday loan, installment loan, car title loan… business-to-consumer [B2C} loan business].

We thoroughly teach online and storefront models.

We provide sample consumer contracts, your State/Province licensing regulations and licensing forms.

We provide specific Chapters devoted to starting, getting customers, loan management software, underwriting consumers, funding your qualified borrowers, collecting your money, websites, marketing, employee hiring, strategies and tactics for learning from your competitors what does and does not work in your geographic area and much, much, more!

For a complete “Table of Contents” to our course, Click the Image:

Payday loan lenders typically require the following for borrowers to qualify :

Generally, payday lenders will require proof that a consumer has:

a regular income

a bank account

a permanent address

Before funding a payday loan, payday lenders will require borrowers to do one of the following:

fill out a form that will allow the lender to withdraw the total loan amount, including fees, directly from your bank account when the loan is due (also called a pre-authorized debit)

provide a post-dated cheque for the total loan amount including fees

Getting money from a payday lender to a qualified borrower

In most cases, the payday lender will deposit money into your bank account via an ACH, a check or, in a storefront environment, give the borrower cash.

However, in some cases, payday lenders may require the borrower to take accept loan proceeds on a prepaid card. It may cost extra to activate and use the card.

Paying back a payday loan

Some payday lenders require consumers to repay the loan at the same location where they got the loan. Others offer online payment. We recommend and teach how a Lender can offer a multitude of payment methods both online and offline.

The Consumer Loan Agreement

Make certain you employ loan management software to compute all fees, payment periods, loan principals, payment schedules, APR’s… We teach all this in our Course! Payday lenders must require their borrowers to sign an agreement that shows your loan costs, including interest, fees, and the due date. FULLY disclose EVERYTHING to the consumer! [Our Course offers names and recommendations to the best companies offering cloud-based software enabling you to run a payday loan business from anywhere in the world!]

A payday loan, installment loan, car title loan… Lenders can make great profits. There are zero guarantees because profitability depends on the Lender.

Payday loans are very expensive compared to other ways of borrowing money. This is because:

Borrowers pay high fees

Borrowers are charged a higher interest rate than on a regular loan or line of credit

Borrowers will have to pay a fee if their cheque or pre-authorized debit doesn’t go through the bank

Borrowers – on average – pay $17.50 per $100 borrowed every two weeks. That’s a 600%+ APR!

So… a borrower gets a payday loan of $300 from their Lender. Two weeks later they pay $52.50 in fees + the $300. At least 40% of these borrowers at a minimum will not pay anything towards the loan principal so the borrower “rolls-over” their loan. Thus another two weeks pass and the borrower pays $52.50 in fees again.

The average payday loan small business has 400 to 600+ customers!

As a Lender, be aware that a payday loan business is not all “peaches and cream!” Whether online, storefront or “blended,” you will have costs, headaches, employees…

But, the potential for earning a SUPERIOR Return on your Investment [ROI] is tremendous.

After all, your inventory is MONEY! You are nor investing in and operating a fruit stand experiencing rotting inventory 😆

With hard work, knowledge, implementation of the latest technology and tactics, Lenders can grow big, earn extraordinary profits and achieve a very nice lifestyle. BUT, at least in the beginning, IT WILL BE HARD WORK!

Figure 1: Comparing the cost of a payday loan with a line of credit, overdraft protection on a chequing account and a cash advance on a credit card (Based on a $300 loan for 14 days)

The costs shown in this example are for illustration purposes only and are based on the following assumptions:

a payday loan costs $17 per $100 that you borrow, which is the same as an annual interest rate of 442%

a line of credit includes a $5 administration fee plus 8% annual interest on the amount you borrow

overdraft protection on a bank account includes a $5 fee plus 21% annual interest on the amount you borrow

a cash advance on a credit card includes a $5 fee plus 23% annual interest on the amount you borrow

What happens to your borrower if they can’t pay back a payday loan on time?

There can be serious consequences if borrowers don’t repay their loan by the due date.

They may include:

the payday lender will charge you a fee if there isn’t enough money in your account

your financial institution may also charge you a fee if there isn’t enough money in your account

the total amount that you owe, including the fees, will continue to accumulate interest

the payday lender could call your friends, relatives or employer in attempts to contact you to collect the money

the payday lender could sell the loan to a collection agency and this could appear on your credit report

the payday lender or collection agency could sue you for the debt

the payday lender or collection agency could seize your property

the payday lender could take money from your paycheques (also called garnishing your wages)

If you can’t make your payday loan payments on time, it can be easy to get stuck in a debt trap.

Infographic: Payday loans: Make sure you pay on time!

What to know to be a payday lender

The total cost of borrowing you can charge. Be sure to find out:

all the fees, charges and interest

the correct date the loan is due

if there is a maximum cost you can charge for a payday loan

What does your competition charge

Fees applied if you’re borrower is unable to pay back their loan on time.

Understand that:

a fee is often charged if your borrower’s cheque or pre-authorized debit is returned due to non-sufficient funds

these fees can range from $20 to $50

many provinces have rules about maximum fees for non-sufficient funds

the amount can be much higher in provinces and territories where the fee is unregulated

Ask if there is a “cooling off” period. This is a period, often a day or two, during which a borrower can cancel the loan with no explanation and without paying any fees. The laws in many provinces protect this right. Make sure to know the “cooling off” period information.

Payday lending rules

Each province and territory has different rules and restrictions around payday lending. However, many online payday lenders aren’t licensed and don’t follow provincial rules designed to protect borrowers.

Canada Fees and penalties

Many provinces regulate payday lending fees and penalties.

NOTE to Payday Loan Lenders! Laws, rules, compliance, regulations are in constant flux! The information below is almost CERTAINLY not current as you read it! Invest in our Course for the latest, most current information!

Table 1 – Payday lending regulations by province

Province

Maximum cost of borrowing for a $100, 2‑week payday loan

Cooling off period to cancel the payday loan

Maximum penalty for a returned cheque or pre-authorized debit

Alberta

$15

2 business days

$25

British Columbia

$15

2 business days

$20

Manitoba

$17

48 hours, excluding Sundays and holidays

$20

New Brunswick

$15

48 hours, excluding Sundays and holidays

$40 (default penalty)

Nova Scotia

$19

Next business day

$40 (default penalty)

Ontario

$15

2 business days

n/a

Prince Edward Island

$25

2 business days

n/a

Saskatchewan

$17

Next business day

$25

Restrictions

In the following provinces, a payday lender can’t extend or roll over a payday loan:

Alberta

British Columbia

New Brunswick

Nova Scotia

Ontario

Saskatchewan

A payday lender can’t ask a borrower to sign a form that transfers your wages directly to them in the following provinces:

Alberta

British Columbia

Manitoba

New Brunswick

Nova Scotia

Ontario

Saskatchewan

Provincial laws define what a payday lender can do when trying to collect a loan. This includes when and how often a payday lender can a borrower and what tactics you can use to get you to pay.

Professor Lisa Servon [watch her interview positioned at the bottom of this Post] got off her butt and worked for months in the trenches “behind the counter” for RiteCheck, a check casher located in the Bronx and for an Oakland based payday loan lender.

Rather than pontificating like the majority of anti-payday loan commentators and academics do, Professor Servon reported to work in a “live” storefront and talked to real people!

She wanted to learn, “Why do these folks CHOOSE payday loans, car title loans, installment loans, and check cashers to help them solve their financial problems. Why not simply pull out their credit card, tap into their savings, click their bank’s smartphone app – or visit their local branch IF one exists – ask friends, family, their church… ”

The results of her experience resulted in a balanced, fair-minded book, The Unbanking of America and the Video Interview below. Yep! Shocks the hell out of me!!

Get Professor Servon’s 2018 book! I have and it’s excellent. It’s balanced. NOT like the Gary Rivlin garbage on Amazon also. His book, “Broke USA: From Pawnshops to Poverty” is more of the same old sad sack “clickbait” stories that lazy media “tools” put out daily.[Here’s a direct link to Amazon OR visit Amazon.com and do a quick search.]

The so-called consumer protectionists [think of the CRL: Center for Responsible Lending], regulators, socialists, leftists fail to get off their duffs and TALK to real customers.

What Profesor Servon was willing to do certainly beats sitting in a faculty room chaise lounge and pontificating about a subject you have zero knowledge about nor personal experience with!

There is NO DOUBT we all have agendas. And these agendas are usually about money. The old saying, “Follow the Money” is a catchphrase popularized by the 1976 docudrama film “All the President’s Men,” which suggests corruption can be brought to light by examining money transfers between parties.

Note: The founders of CRL are Herbert Sandler and his wife Marion Sandler, founders of the Sandler Foundation. The Sandlers’ have been heavily criticized for their role in the 2008 financial crisis. Their California Savings and Loan financial company, Golden West, was one of the many banks to offer the adjustable-rate mortgages that were blamed for the subprime mortgage crisis. The Sandlers’ ties to the financial crisis were detailed by CBS’s 60 Minutes.

An investigation by Politico revealed CRL had a heavy role in helping the CFPB draft new regulations on payday loans. According to POLITICO, “The group regularly sent over policy papers, traded emails and met multiple times with top officials responsible for drafting the rule. At the same time, the group’s financial services business, Self Help Credit Union, was pushing CFPB to support its own small-dollar loan product with a much lower interest rate as an alternative to payday loans.”[6]

An investigation by the House Oversight Committee[9] found that the Federal Deposit and Insurance Commission took a prominent role in Operation Choke Point, an interagency initiative to pressure banks to stop providing business services to industries such as payment processors, firearms sellers, payday lenders, etc. As members of the FDIC’s Advisory Committee on Economic Inclusion, CRL board member Wade Henderson pushed agency leadership to crack down on the payday lending industry—one of the industries targeted by Operation Choke Point. Additionally, according to emails uncovered by the Oversight investigation, Mark Pearce (former CRL president and current director of FDIC’s Division of Depositor and Consumer Protection), was exploring ways for FDIC to “get at payday lending.” The report found Pearce used his position to push for stringent regulations on the payday lending industry.[10] CRL praised efforts by Operation Choke Point to increase regulations on payday lenders.[11]

It’s notable too that Martin Eakes was a Co-Founder of CRL in 1998. Mr. Martin Daniel Eakes is an American economic development strategist and credit union CEO. [Do you know credit unions do not have to pay taxes?]

Do you “get” it? Banks and credit unions DO NOT LIKE the payday loan industry!They are competitors. Banks and credit unions have access to cheap money thanks to the Federal Reserve and tax breaks. In other words, their cost of capital is far less than that of Lenders offering payday loans, title loans, installment loans, line-of-credit loans… to the very low FICO/no credit/thin-file consumers who are in MOST NEED of access to fast, no-hassle, small-dollar loans.

This explains why the 36% APR theme is becoming prevalent today! If a 36% APR is mandated nationwide, only Lenders large enough to collaborate with banks via “the bank model” – exportation of interest rates across state lines, and credit unions have a shot at the 40% of USA households unable to access $400 cash in a financial emergency and the 70% who cannot access $1000 cash! These institutions will own these folks. Provide capital to “the big boys” or continue to collect BILLIONS of Dollars in NSF fees!

Thankfully, there is another option. Federally recognized Native American Indian tribes such as Leaning Rock Finance have entered the fray via E-commerce. Tribes who previously were experiencing extreme poverty because our government placed them on reservations deemed worthless, have the ability today to participate in offering a multitude of loan products to consumers via the Internet. Much like the “bank model,” Indian Country has hired sophisticated, experienced, financial savants and 3rd party vendors to provide a bit of competition for the banks. For more than a few tribes, this development has turned their economies around significantly enabling the tribes to create jobs, build schools, health care facilities, alcohol/drug abuse programs and much, much more.

Your typical mom-and-pop payday, installment… small-dollar loan providers cannot acquire, underwrite, fund, and service these sub-prime borrowers under the thumb of a 36% APR cap! [Not unless these lenders figure out how to “stack” ancillary fees on top of 36% APR loans much like the 3 primary supporters of California AB539 have accomplished.]

Yes, I know! A 36% APR appears high at first glance. Let’s examine the numbers. $300 borrowed for 12 months at 36% = $108/year in fees; IF the borrower really makes their payments. [Many sub-prime customers require a little prodding.] Continuing the math, that $108/yr = $9/month interest. Now the “big boys,” the publicly traded companies like Enova, Curo, Elevate, OneMain, WRLD… filings indicate their 1st-time customer acquisition costs are approx. $280. That’s just to acquire a customer. They still must underwrite, decision, fund, service, collect… And as I’ve written before, this 36% APR theme originated in the early 1900’s. Know that a $300 loan in 1900 is equivalent to a $7,000 loan today! So… that’s their plan [banks]. MUCH higher loan principals – no way is a bank or credit union going to fund a $300 loan. And, minimum 12 to 60-month loan terms! Say goodbye to a quick $300 until your next payday!

Do you understand that the same customers who bounce checks [NSF’s] are payday loan customers?

According to Federal Deposit Insurance Corporation (FDIC) data and the New York Post, overdraft fees [NSF’s] have reached their highest level since 2009, which was at the end of the Great Recession. Consumers paid $34.3 billion in overdraft fees during 2017 compared to $33.3 billion in 2016, The New York Post reported.

Despite the increase, consumers aren’t, in fact, overdrawing their accounts. Instead, Moebs Services says the uptick was caused by credit unions increasing their overdraft fees. Overall, average overdraft fees at banks have risen from $20 in 2000 to $30 in 2017. Over that same time frame, the average overdraft fee at credit unions has increased from $15 in 2000 to $29 in 2017.

In August of 2017, the CFPB released a study that exposed the extent to which large banks’ abusive overdraft fees drain working families’ checking accounts. The study found that nearly 80% of bank overdraft and NSF are borne by only 8% of account holders, who incur ten or more fees per year, with many of those customers paying far more. For one group of hard-hit consumers, the median number of overdraft fees was 37, nearly $1,300 annually. The study also confirmed that overdraft fees on debit cards can lead to extremely high cumulative fees for consumers.

Opted-in frequent overdrafters typically pay almost $450 more in fees: The typical opted-in frequent overdrafter has 22 overdrafts compared to 18 for frequent overdrafters who have not opted in. However, the opted-in frequent overdrafter typically incurs 18 overdraft fees over a year, compared to only five for the typical frequent overdrafter who has not opted in. With a typical overdraft fee of $34, this means that the median opted-in frequent overdrafter pays almost $450 more in overdraft fees than someone who has not.

Frequent overdrafters have low or no credit scores: Consumers who overdraft frequently have median credit scores of less than 600, well below what is considered to be a subprime score. Consumers with lower scores generally have difficulty obtaining new credit. Roughly 20 percent of frequent overdrafters do not have a credit score in the data that was studied. In many respects, frequent overdrafters without a credit score appear even worse off financially than other frequent overdrafters.

Anti-payday loan protagonists refer to APR’s consistently when comparing payday loans to bank and credit card products. The APR on a bounced check approaches 17,000%! Do you know that?

According to the CFPB Report, most overdraft fees are incurred by debit card transactions of $24 or less and are repaid within three days. Consider overdraft fees in a lending context: If you were to take out a $24 standard loan and pay an additional $34 to borrow the funds for three days, this loan would have a 17,000% APR.

I’ve “worked the counter.” There certainly are some “bad” operators in our industry. The same goes for virtually all industries including banking, Wall Street, politics, and your local yogurt shop.

There are a LOT of nuances regarding this subject.

If you really care, get out there. Do something. Contribute. Check out Amscot Financial in Florida [No affiliation except I know the father and sons.] They are a great example of our industry giving back to their community.

Finally, for those of you who think outlawing these businesses is the answer? You cannot legislate demand away. Do you think banks are the answer? They fund our businesses. They provide credit lines to Lenders. They securitize the portfolios of our publicly traded companies and more. Banks get nearly free capital from the FED, leverage the hell out of it and make serious money on the “spread.” Banks hold up checks, as mentioned in this video from Thursday through Wednesday intentionally so they can game the “float.”

Watch this Professor Lisa Servon interview below! Get her book. I guarantee it’s worth your time whether you’re a lender, a borrower, an advocate, a regulator, a legislator, or simply someone with a desire to be informed!

Finally, if you’re interested in joining this party,CLICK HEREto grab a copy of our ‘bible,” the latest version of “How to Start or Improve a Consumer Loan Business.” Get it delivered to your Inbox immediately. Read it. Study it. Then call me: Jer 702-208-6736. Let’s explore…

Available: Experienced Operations Manager: Tribal Lending, Call Center, Marketing, Collections…

Nici C. is an experienced Operations Manager/Team Member in the Subprime as well as Tribal Lending Industry seeking her next opportunity.

With 10+ years of small-dollar lending experience, Nici possesses exceptional skills in call center and operations management, marketing campaign management, CRM, collections, complaint handling and resolution, staff development, fraud investigation and monitoring, quality assurance, as well as startup experience. Nici will consider ALL working environments including remote, part-time, project oriented, full-time… She’s currently based in Atlanta.

What LMS providers is she experienced with?EPIC, TranDotCom, Infinity

Which CRA’s? Why use one or two vendors vs another?Experience in dealing with vendors to change control files and manage data issues. Worked with Clarity, Factor Trust, Data X and Decision Logic

Which underwriting 3rd party vendors has she worked with?Clarity, DataX, IDology, Factor Trust, LexisNexis

Would she say she has “relationships – first name basis” with the network of vendors servicing our space? Can she pick up the phone and get an issue handled?Yes

Can she write about the industry?Yes

In-depth analysis? Trends? Niches within the industry?Yes

From industry trends to customer acquisition through underwriting, processing, funding methodologies, vendor selection, collection strategies…Yes

Experienced in what, if any marketing channels/customer acquisition?Email, social media, voicemail drops, direct mailing…

Is she familiar with and able to provide commentary and insight regarding typical KPI’s? How to improve them? For both de novo and seasoned?Yes

Any title loan B2C experience?No

Which tribes has she worked for? Several! Has NDA’s in place. [She’s discreet!] Has also worked with offshore and state by state lenders.

Languages?English

IMPORTANT: Is she a skilled content writer?Yes

Ever hear of Podium?Yes

Google Adwords skill set?YesWorkarounds for their PDL policies?YesSame for FB?Yes

SEO/SEM?Yes

Bank relationships? Amenable to B & M’s? Tribes?No [Dear reader: Click here for a tribe: Leaning Rock Finance

Know WordPress backend?Yes

HTML?Yes

Photoshop?Yes

FB? Yes

Instagram?Yes

Twitter?Yes

Developing direct mail pieces?Yes

Familiar with the latest AI and automation platforms?Yes

Enjoys nothing better than to go to bed at night and read the latest judicial wins by the companies employing the sovereign nation [tribal model] and the superior financial returns reported by ENVA, CURO, ONEMAIN FINANCIAL, WRLD, CACC, ELVT… quarterly earnings reports along with the great work performed by our industry associations including NAFSA, OLA, CFSA, FISCA..?Yes {Man, this girl is as sick as Jer}

Tell me more about “fraud investigation.”Monitoring accounts for suspicious activity; investigating fraudulent transactions and dispute filing/resolution in the prepaid card industry.

Does she live and breathe our industry?Yes

Fintech aware/oriented?Yes

Can’t get enough. Is she crazy like us?Yes!

How does she react if called a “loan shark?”First, be empathetic then respond with facts as it pertains to terms and conditions/signed agreement.

What are her income requirements?Open to negotiations. Depends on the gig!

What’s the largest headcount she’s managed?77

Portfolio size? Transaction monthly volume?Managed a Team doing 100 loans a day, Managed a Collections Team of 20 and a origination team of 50, managed QA departments.

Insurance requirements?Yes

Able/willing to attend the Assoc. Conventions?Yes

Would you consider her more of an assistant? Assigned tasks and completes them? Or a creator who can join disparate ideas and combine them leading to 100X outcomes for her Team?Well-versed; ability to do both!

In an ideal world, what would Nici PREFER to be doing?In an ideal world, Nici would prefer to be working with a PDL Company where she can continue to grow/learn and is seen as an asset by utilizing her current skills/knowledge to grow the portfolio.

Now if you’re “old school,” like I was back in the day, this will likely piss you off!

After all, to build your consumer loan business it’s likely you approached the launch of your payday loan business, your installment loan business, your car title loan business, your pawnshop business… whatever you choose to call it, and plodded through your State licensing process. You then selected a loan management software provider, integrated with ACH and debit card providers, struggled to get a bank account opened… and on and on. Just to get a State license can kill 30 – 90 days+. Oh, you’re a Lender so let’s not forget to get your Bond! And your lawyer, your consumer loan contracts… Of course, by collaborating with a federally recognized Native American Indian tribe you could get set up within 30 days and loan in 37+ States.

Why do I suspect the following Forbes piece will upset you? Because these new Fintech Lenders “don’t need no stinking badges” – I mean licenses. [Shout out to Clint Eastwood in “The Good, the Bad and the Ugly.” Great movie and soundtrack!]

According to the Forbes article:

“Quo relies on using AI to sort through a user’s financial transactions to understand their spending habits.

Once a user’s economic history is compiled and interpreted, the startup sends a debit card to the user for financial use.

The debit card allows access to two types of loans via a monthly subscription: $5.99/month for $400 at 5% APR or $9.99/month for $700 at 2% APR.

Those interest rates are dramatically lower compared to credit cards and payday loans.

The startup providing these loans from a small-monthly fee with borrower-friendly APRs reflects their mission of not wanting their users to be in debt.

Unlike the conventional credit business models, profit is not made by keeping users spending and perpetually in debt to pay interest, but by getting them out of debt to build savings.

These loans come with user-specified constraints, such as the money only being used at merchants that are relevant to the purpose of the loan. If someone is taking out the loan to make a car payment, then the user could only spend that money to pay off the vehicle for that month. More importantly, if a user falls behind on their loan repayment, Quo is able to restructure the loan in real-time to adjust to a person’s immediate financial constraints.”

Shout out to the author of this piece on Forbes! Frederick Daso Contributor. “I write about college students and recent graduates founding startups.”

PS: Want to know how to jerry-rig and integrate all the “plug-n-play” platforms and services available today for launching a consumer lending company “on the cheap?” Grab a copy of our 2020 “bible:”The Business of Lending to the Masses. Here’s the “Table of Contents.”

By Jer AylesCURO reports $300M+ quarter. Enova reports a $300M+ quarter. Lendup reports $2B. On and on and on! Demand by consumers in all economic brackets through the roof unabated! I could name dozens of additional lenders struggling to meet demand. In January 2019, Dave.com had 1,000,000 subscribers paying a $1/month subscriber fee JUST TO BELONG. By September 2019, Dave.com had 5, 000,000 paying $1/month! Earnin. Cash America. Elevate. First Cash. Four Oaks. One Main Holdings. Does it ever end?

How to Start a Loan Business

Billions of dollars are lent every month to U.S. consumers! And let’s not ignore the Native American Indian tribe, online lenders! LeaningRockFinance.com. LDF is said to have 20 portfolios totaling $80,000,000 on the street.

From Yahoo Finance: “LendUp, the company whose goal is to make financial health a reality for all, announced today it has issued over $2 billion in consumer financing through its digital lending platform. Since 2012, LendUp has provided more than 6.5 million loans, with an average loan value of approximately $300. The company continues its commitment to providing more people with greater access to consumer credit and financial services.

“We’re very proud of this significant lending accomplishment, the progress we’ve made in driving disciplined, profitable, and sustainable growth, and our role as a standard-bearer for responsible and inclusive lending and banking,” said Anu Shultes, CEO of LendUp.

Named by CB Insights as one of the startups disrupting the retail banking value chain, LendUp helped to pioneer embedded financial education as a model to support more than half of Americans who are underserved by traditional credit and banking markets. The company combines its education programs with access to microfinance solutions such as short-term installment loans—which can help end the need for these consumers to take on more costly credit solutions, including traditional payday loans, title loans, and overdraft protection.

“Through our lending, education, and savings programs, we’ve helped customers raise their credit profiles by hundreds of thousands of points cumulatively and saved them hundreds of millions of dollars in interest and fees from much higher cost products. While there’s much more for us to accomplish, this milestone is a real testament to the impact that financial service providers like LendUp can and should have on the market,” added Shultes.

In January 2019, the company announced the spinoff of its credit card business into a new entity, Mission Lane, allowing LendUp to focus on its core lending, experiential education, and cost-savings programs that have helped to put more people on a path to financial health. LendUp customers have taken more than two million courses through the company’s gamified financial education platform that teaches them better ways to manage their money, establish a credit profile, and develop stronger financial behaviors—like saving for an emergency fund.

Anu Shultes Marks One-Year Anniversary as CEO

Shultes, one of the few female CEOs leading a major fintech lender.

The future looks GREAT for lenders! Need help getting started? Are you a Lender today in need of expert help to improve your operations? Reach out! Get a copy of our “bible” or schedule a call: Clarity.fm Calendar

CURO, a publicly traded lender, originates $1 Billion dollars [+/-] in consumer loans every 3 months. They have approximately a 3% market share. What's this mean for you? OPPORTUNITY!

The near-prime will soon be the subprime. Demand for loans of $500 to $5000+ continues to escalate. Opportunities are boundless for lenders.

As a lender, your inventory is MONEY! Not tulips dying. Not bananas rotting. The 99% will ALWAYS need money. Debt is the reality of living in America.

What do we do? We teach entrepreneurs how to lend money to the Masses. We lend money. We offer Courses, consulting, investments, access to our vast network of vendors, lawyers, Instant Bank Verification, payment processors, website designers, and underwriting...

We are 100% focused on the business of lending to the masses! Installment loans, car title loans, payday loans, line of credit loans...