Subprime Loan Business in 2026: Demand Is Strong, But Weak Paper Kills Profit

2026 Operator Briefing for Subprime Lenders Subprime Loan Business in 2026. Demand is Strong, but Weak Paper Kills Profit Payday, car title, installment, and Texas CAB lenders still have demand. The lenders who will win will approve better, document better, collect earlier, and stop pretending volume alone is strategy. Get The Bible Schedule Free Discovery […]

Texas CABs: The Complaint Wave Is Here. Audit Your Disclosures Before Someone Does It For You.

Texas Appleseed is back. Ann Baddour’s Fair Financial Services Project has been gunning for payday and auto title lending for years. If you’re surprised complaints are hitting CABs again, you haven’t been paying attention. Here’s the truth: a complaint is an allegation, not a verdict. But allegations still cost you time, money, focus, and operational […]

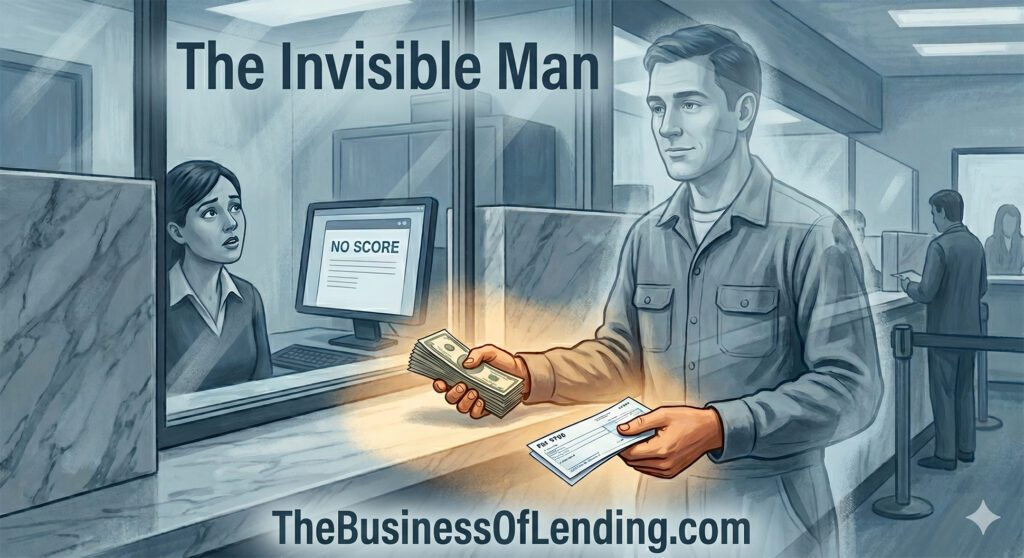

No Score. No Deal. No Logic: The Edge in Subprime Lending (What’s Working in 2026)

FICO Didn’t Decline Your Borrower. Your Data Stack Did. You didn’t lose that loan because the borrower was a bad bet. You lost it because your system had no way to see them. “No score. No deal.” That’s not a risk decision. That’s a data problem wearing a policy costume. Here’s the truth: FICO was […]

Best Practices for Underwriting Subprime Loans in 2026

Identity verification matters, but it is not underwriting. It only tells you the applicant exists. It does not tell you how they behave after funding. Real subprime underwriting looks at cashflow, volatility, repeat behavior, fraud signals, and timing. If your model begins and ends with ID, income, and a credit pull, you may be screening […]

Free, Try My A.I. Clone for Subprime Lending Operators

Unveiling This Strategy: A Conversation With My A.I. Clone What you’re reading here came from a conversation between one of my clients and my A.I. clone. That is not a gimmick. That is the point. My clone is trained to break down complex lending questions into practical strategy, clear thinking, and real-world next steps. It […]

Subprime Lending KPIs That Tell You If You Are Actually Profitable

TL;DR: Most subprime lenders think they are profitable because they track the wrong numbers. The four KPIs that actually matter are charge-off rate by vintage, roll rate by loan type, cost per funded loan, and net yield after defaults. These numbers show whether your underwriting, collections, and unit economics are really working before the damage […]

The USA wide ‘Predatory Lending Elimination Act’ Doesn’t Eliminate Predatory Lending. It Eliminates Lending.

170 organizations just asked Congress to make it illegal for you to serve the borrower no one else will touch. Senate Bill S3793, the “Predatory Lending Elimination Act,” would slam a 36% APR cap on virtually every consumer credit product in America. Credit cards, installment loans, car title loans, payday loans… All of it. Senator […]

The Rule That Was Supposed to Save the Poor But Made Them Poorer

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Online vs. Storefront Lending in 2026: Where Profits (and Pitfalls) Hide

Ever had that “big choice” moment, double down on your storefronts, or swing fully into digital? I was asked three times last week: “Jer, what’s really working in 2026, boots on the ground or all-in online?” Let’s get blunt. Every subprime loan operator staring down a margin squeeze or new compliance fire wants a silver […]