Subprime Lenders Lose More Money to Caution Than They Ever Lose to Default

They just never see it on a spreadsheet. Quick answer:Most subprime lenders do not get crushed by default. They get crushed by caution. When your “book” is undercapitalized, you start making cash decisions that look like risk decisions. You tighten, you stall, and the biggest loss never hits the P&L. It walks out the door […]

Payday, Title, and Installment Loan Demand in 2026: Where Profits Are Headed

Is small-dollar loan demand still strong in 2026? See what the latest public data suggests about payday, title, installment, and line-of-credit loans, plus the underwriting and acquisition shifts that protect net profit.

Subprime Lending’s Perfect Storm:

“Demand Up, Regs Down, Profits Skyrocketing” A Golden Moment for Subprime Lenders The Clock Is Ticking. The Opportunity Is Now. I’ve spent the last 90 days assembling the ultimate subprime lending playbook for 2025/2026. This playbook is designed for lenders specializing in payday loans, car title loans, and installment loans. The data is explosive. […]

BNPL for Beans: Why Your Borrowers Are Financing Their Frosted Flakes and What That Means for YOUR Loan Portfolio

Remember when Buy Now, Pay Later (BNPL) was the shiny toy Gen‑Z used to snag Yeezys and Pelotons? Fast‑forward to 2025, and one in four BNPL users now swipe the four‑pay button at checkout for milk, eggs, and baby formula – up from just 14 % last year, according to LendingTree’s April survey(lendingtree.com). At the same time, 41 % […]

What’s Your Biggest Challenge Today?

Loading…

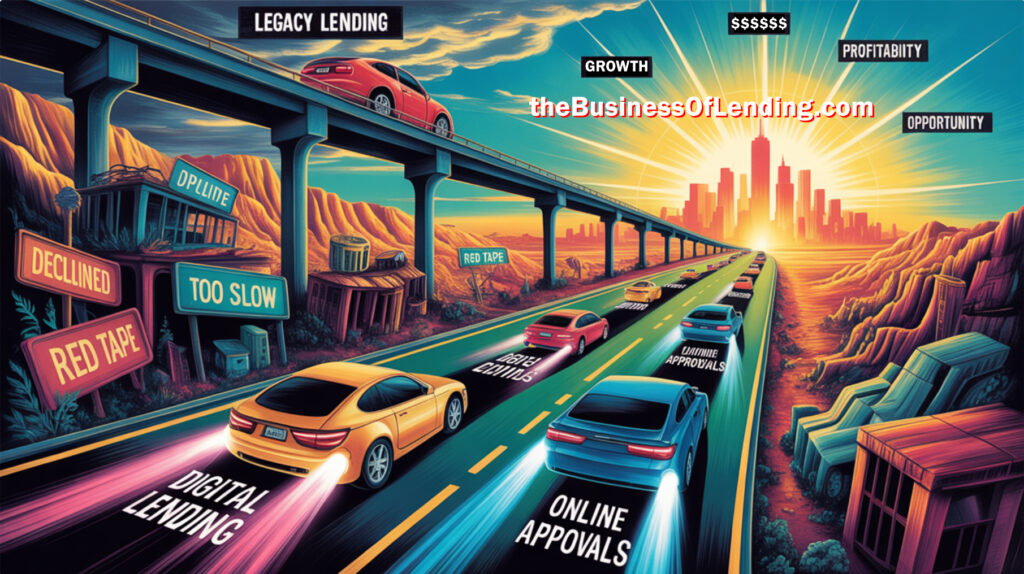

Why Now Is the Best Time in 20 Years to Start or Scale Your Subprime Loan Business

Subprime Loan Business: 1. America Is Drowning in Consumer Debt 2. Big Banks and Credit Unions Want Nothing to Do with Them 3. Digital Lending Is the New Frontier 4. The Margins Are Insane 5. The TAM Is Jaw-Dropping 6. Investors Are Paying Attention 7. Compliance Is No Longer the Barrier It Used to Be […]

How to Secure Capital and Build Strategic Partnerships in the Subprime Lending Industry

Build a Subprime Lending Empire Without Begging for Money Think you need Wall Street to fund your next big move? Think again. The Real Money in Subprime Lending Isn’t Where You Think. Forget what you’ve been told. You don’t need a Wall Street zip code to raise capital or the old boys’ club to open […]

7 Tactical Moves to Safely Scale Your Subprime Loan Portfolio in 2025

Let’s cut to the chase! The Demand Is Real. The Danger Is, Too. Every day, subprime lenders leave millions on the table; or worse, lose it to defaults and regulators. There’s a right way to scale. And a reckless way. This isn’t theory. It’s the exact playbook smart operators are using to grow fast without […]

How to Lend to Strangers Without Losing Your Shirt

A Field Tested Review of Unsecured Lending Risk Management (2nd Edition) by Frank Tian This Book Is Written for People Who Actually Lend Money A Field Tested Review of Unsecured Lending Risk Management (2nd Edition) by Frank Tian If you’re in the business of lending money to subprime consumers, you already know the stakes: high […]