By: Jer Ayles – Trihouse Consulting.

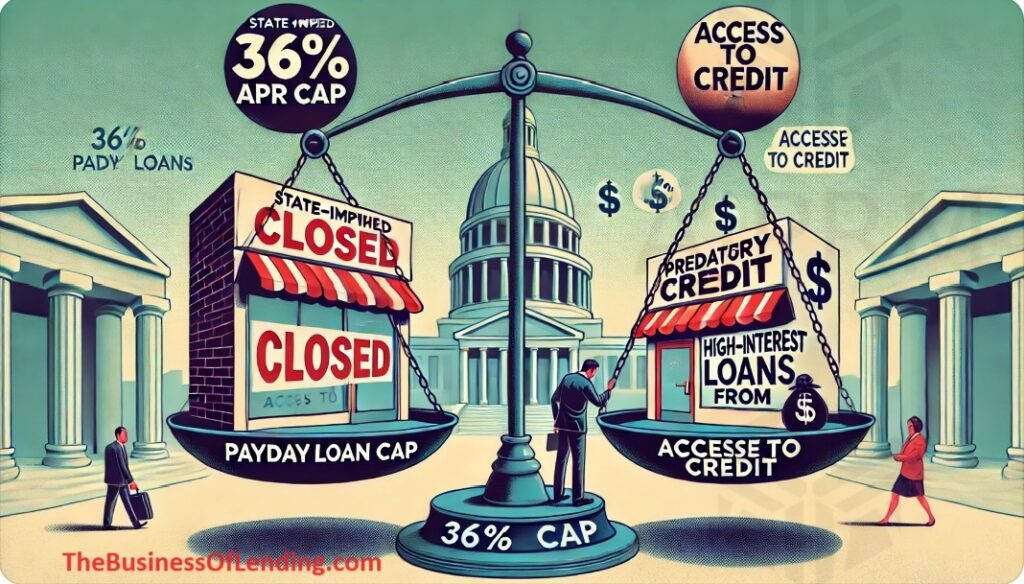

The continuing trend of states imposing a 36% APR cap on payday loans is touted as a consumer protection measure. However, this well-intentioned policy has unintended consequences that actually harms the very people it aims to help. Let’s explore why payday loan products are better than the state implementing a 36% APR cap thus driving payday loan lenders out of the state and thereby eliminating subprime consumer access to credit.

The Fallout of the 36% APR Cap: A Case Study of Illinois

In Illinois, the imposition of a 36% APR cap has resulted in a dramatic reduction in the availability of small-dollar loans. A comprehensive study found that this restriction decreased the number of loans to subprime borrowers by 44% while increasing the average loan size by 40%.

This means that fewer consumers are getting the loans they need, and those who do are forced to borrow larger amounts, which often leads to greater financial strain.

The Demand for Short-Term Credit Persists

The demand for short-term credit does not disappear with the imposition of an APR cap. Instead, it forces consumers to seek alternative sources, often leading them to unregulated and potentially predatory lenders.

Illegal lenders, who operate without oversight, typically charge exorbitant rates far exceeding the 36% cap, putting consumers in even more precarious financial positions.

Misguided Legislation and Unintended Consequences

Proponents of the 36% APR cap argue that it protects consumers from high-interest rates. However, this perspective fails to consider the operational costs and risks associated with small-dollar lending.

In 1916, it was determined that an annual interest rate of about 36% was necessary to cover the costs and risks of small-dollar loans. Today, with inflation and increased operational costs, this rate is no longer viable, especially for short-term loans.

Evidence from Other States

Colorado’s experience corroborates Illinois’s findings. Data from Colorado’s attorney general confirmed that interest rate caps reduce access to credit for nonprime consumers.

Comparatively, states like Utah and Missouri, which have fewer restrictions on small-dollar lending, have not seen the same reduction in credit availability.

The Bankruptcy Boom

Recent data indicates a significant rise in bankruptcy filings, a trend that has persisted for 19 consecutive months.

Consumers, unable to secure necessary short-term credit, are increasingly turning to bankruptcy as a last resort.

This not only devastates their credit scores but also hampers their financial recovery and stability.

Addressing Opposing Viewpoints

Critics of high-interest payday loans argue that these products trap consumers in a cycle of debt.

While this is a valid concern, the solution lies not in capping interest rates but in improving financial literacy and ensuring transparent lending practices.

Consumers should have the option to choose loans that meet their needs, with full awareness of the terms and conditions.

Our elected officials, and more importantly, their staff members, need to engage directly with their constituents to understand their financial challenges better. It is naïve to ignore the fact that lobbying organizations and so-called non-profits often have their own agendas.

A Call for Balanced Regulation

Rather than imposing blanket APR caps, regulators should focus on creating a balanced framework that protects consumers while ensuring access to credit.

This includes setting reasonable interest rates that reflect the costs and risks of lending, coupled with robust consumer protection measures to prevent abusive practices.

Encouraging a Dialogue

This topic is undoubtedly controversial, and we welcome diverse opinions. Share your thoughts in the comments below and join the conversation. How can we better balance consumer protection with the need for accessible credit?

Questions? Need help? Introductions?

Reach out to Jer at : TrihouseConsulting@gmail.com

4-WAYS I CAN HELP YOU!

Grab a copy of our “bible:” Learn More

Brainstorm: Learn More

The Business of Lending: Learn More

Free Bi-Monthly Newsletter: Learn More