The 36% APR Cap: What Actually Happens When You Pull the Ladder

TL;DR A 36% APR cap sounds like protection. It isn’t. The math doesn’t work at $4.15 in revenue on a $300 two-week loan. Lenders know it. So they leave. The borrower still has the emergency. The car still needs fixing. Tuesday still comes. They just have fewer legal options and more expensive illegal ones. You […]

New York STOP Act Kills Tip-Based Lending Models and Told the Entire “Tip-Based Lending” Industry to Drop Dead

The STOP Act is coming. And it’s not just New York’s problem. Here’s what happened: New York legislators introduced a bill that treats every dollar a consumer pays for a wage advance, tips, expedited fees, and membership charges as a finance charge. Slap those numbers into the APR formula, and suddenly the “no-interest” earned wage apps […]

The 12 States Where Lenders Are Making a Killing (And Why You’re Not There Yet)

Where to Expand Next: APR Realities by State (as of 2025/26) I’ve created a field ops plan: map the actual APR ceilings, CAB options, and enforcement heat, then rank states so you stop chasing dead markets. Below is a tight, evidence‑based playbook you can act on now. 1) Key Challenges (with data) Regulatory volatility & patchwork caps […]

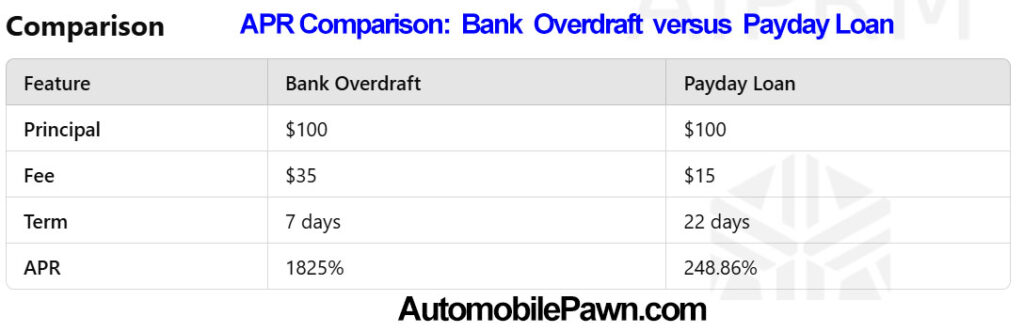

Bank Overdraft Limits: The Golden Window for Subprime Lenders

The finalized rule from the CFPB, capping overdraft fees and reclassifying some as loans, will significantly impact both traditional banks and the subprime lending industry. Here’s a detailed analysis: Overview of the Legislation Options for Fees: Banks can now: Charge a flat fee of $5. Charge fees to cover costs/losses. Structure fees as disclosed loans, […]

When Rules Backfire: The Unintended Fallout of APR Caps on Subprime Borrowers

When well-meaning regulations collide with the realities of financial need, the fallout can be as unexpected as it is impactful. Imagine Joe, a single parent caught off-guard by a medical emergency seeking a $500 loan to cover urgent expenses. Now, picture the lender, bound by a 36% APR cap, trying to offer that help while […]

The Truth About State-Imposed 36% APR Caps

By: Jer Ayles – Trihouse Consulting. The continuing trend of states imposing a 36% APR cap on payday loans is touted as a consumer protection measure. However, this well-intentioned policy has unintended consequences that actually harms the very people it aims to help. Let’s explore why payday loan products are better than the state implementing […]

Must-Read: The Hidden Consequences of the Senate’s 36% APR Loan Cap Bill!

Predatory Lending Elimination Act (S. 3549) Analyzing the Impact of the Proposed 36% APR Cap on Consumer Loans IntroductionThe U.S. Senate is considering a significant legislative move that could redefine the consumer lending landscape in America. The “Predatory Lending Elimination Act” seeks to implement a nationwide 36% annual percentage rate (APR) cap on all loan […]