The Dave.com Trap: A Blueprint for Ethical and Profitable Subprime Lending

Executive Summary: A Wake-Up Call for Subprime Lenders Subprime Dave Inc., a trailblazer in the online cash advance industry, now finds itself in the crosshairs of regulatory bodies like the FTC and Justice Department. Accusations of deceptive marketing, hidden fees, and ethical missteps have laid bare not just the company’s practices but systemic vulnerabilities in […]

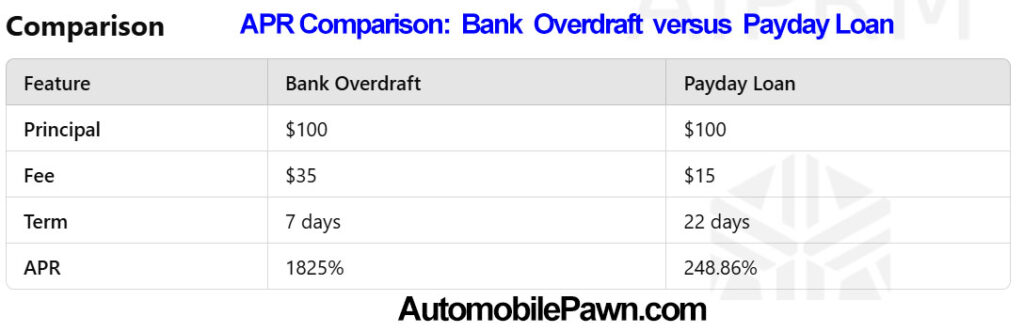

Bank Overdraft Limits: The Golden Window for Subprime Lenders

The finalized rule from the CFPB, capping overdraft fees and reclassifying some as loans, will significantly impact both traditional banks and the subprime lending industry. Here’s a detailed analysis: Overview of the Legislation Options for Fees: Banks can now: Charge a flat fee of $5. Charge fees to cover costs/losses. Structure fees as disclosed loans, […]

When Rules Backfire: The Unintended Fallout of APR Caps on Subprime Borrowers

When well-meaning regulations collide with the realities of financial need, the fallout can be as unexpected as it is impactful. Imagine Joe, a single parent caught off-guard by a medical emergency seeking a $500 loan to cover urgent expenses. Now, picture the lender, bound by a 36% APR cap, trying to offer that help while […]

Why Every Subprime Lender Needs a Loan Shark in Their Marketing Tank

Learn More: LocalListingSuccess@gmail.com Loan Shark Larry Copywriting Dynamo with a Fin for Financial Persuasion ObjectiveTo navigate the murky waters of consumer finance and surface as the ultimate financial copywriting predator. About MeWith a nose for storytelling sharper than a shark’s tooth, I thrive on crafting compelling narratives that bridge the gap between lenders and borrowers. […]

The $100 Ripple Effect: Lessons for Subprime Lenders in Serving Credit-Challenged Consumers

A bald, bearded stranger stopped in a small town and walked into its modest hotel to inquire about a room. Before inspecting the premises, he left a $100 bill as a deposit with the hotel owner. What followed next was extraordinary. The hotel owner, clutching the $100, rushed next door to pay his overdue grocery […]

Trump, Jobs, and Subprime Loans: Why America’s Lenders Are Set to Thrive

Trump is back in the White House. It’s an exciting time for running small loan businesses, and I couldn’t be more optimistic. For those of us working day in and day out to provide honest, reliable credit to credit challenged folks who need it most, having a President who values hard-working Americans is a breath […]

Cracking the Code: How World Acceptance Corporation Achieved Extraordinary Profits in Subprime Lending

As a lender, owner, operator, capital provider and consultant analyzing World Acceptance Corporation’s latest earnings report, I see several positive trends and opportunities for lenders operating in the subprime consumer lending space, particularly those focusing on small-dollar loans for customers facing sudden financial emergencies.. Market Opportunity World Acceptance Corporation’s results indicate a growing demand for […]

Ever Had a French Fry Burn? That’s What Your Financial Restrictions Feel Like.

Let the Market Decide: A Lesson from the Counter Jer, ever had a french fry burn? Doesn’t feel great, does it? But sometimes, it takes that kind of sting to wake folks up. Those who want to tell us how best to handle our finances—our “overlords”—could learn a thing or two from actually working the […]

To those who criticize subprime lenders, let’s be real about the alternatives for financially challenged consumers.

Why Subprime Lending Isn’t the Villain You Think It Is Yes, subprime lenders charge high fees, but consider the reality: more than 60% of U.S. workers live paycheck to paycheck, often facing sudden financial crises with nowhere else to turn. When their car breaks down, a medical bill hits, or rent is due, what options […]