The Federal Communications Commission (FCC) has announced a one-year postponement of its one-to-one consent rule, shifting the implementation date from January 27, 2025, to January 26, 2026.

This delay provides subprime lenders with valuable time to adjust their practices and understand the implications of this significant regulatory change.

The rule requires payday loan, car title loan, installment loan, line-of-credit loan businesses to obtain prior express written consent from consumers before contacting them using automated systems or pre-recorded voices 6. This means that instead of relying on a single consent given to a lead generator, each individual lender must obtain separate consent from the consumer before making any marketing calls or sending texts

This rule change is a direct response to the “lead generator loophole,” which allowed businesses to use a single consumer consent to share their information with multiple companies, often resulting in a flood of unwanted communications 8. By requiring one-to-one consent, the FCC aims to give consumers greater control over their personal information and reduce the volume of unsolicited marketing calls and texts.

Impact on Subprime Lenders

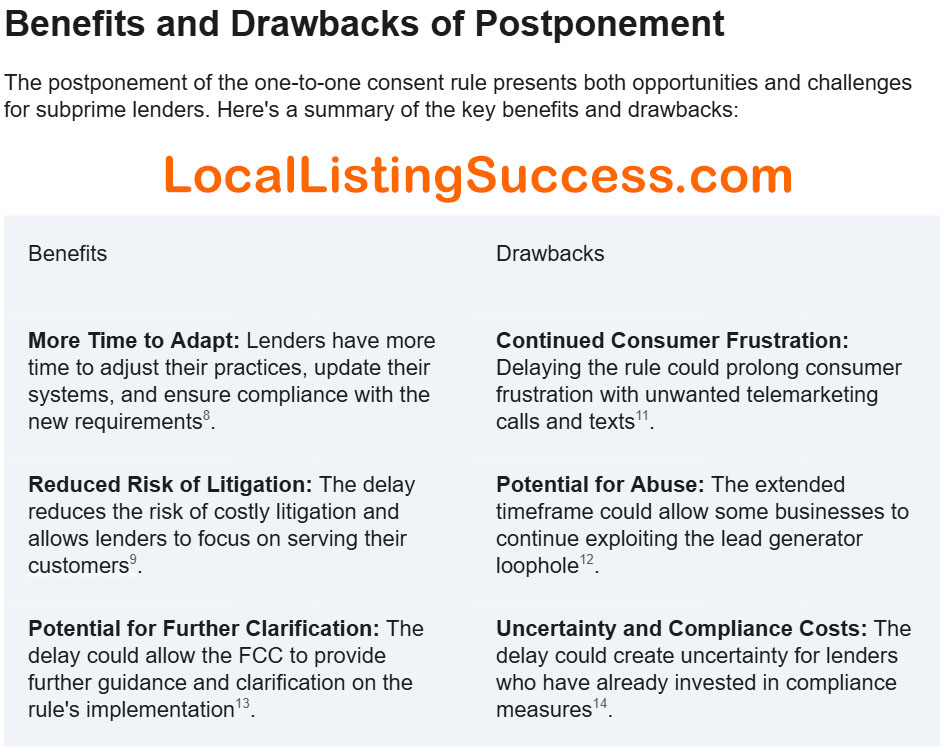

The one-to-one consent rule has the potential to significantly reshape the subprime lending landscape. While the postponement provides some breathing room, lenders need to understand the long-term implications and proactively prepare for the eventual implementation of the rule. Here’s a closer look at the potential impacts:

- Increased Communication Restrictions: The rule limits lenders’ ability to contact consumers using automated systems or pre-recorded voices without obtaining explicit consent for each individual lender 8. This could make it more challenging to connect with potential borrowers, especially those who may not actively seek out loans but could benefit from them.

- Higher Compliance Burdens: Subprime lenders will need to implement new procedures to ensure compliance with the one-to-one consent rule, including updating consent forms, obtaining and storing consent records, and training staff on the new requirements 9. This could increase administrative burdens and compliance costs, potentially diverting resources away from core lending activities.

- Increased Costs: Obtaining individual consent for each lender could be more time-consuming and expensive than relying on shared consent obtained through lead generators 10. This could increase the cost of acquiring leads, potentially impacting the affordability of loans for consumers.

- Lead Quality and Brand Recognition: While the cost per lead may increase, the quality of leads could also improve. With one-to-one consent, lenders will be contacting consumers who have specifically expressed interest in their services, leading to more targeted and higher-value leads 10. This shift could also make brand trust and recognition more important, as consumers will be more selective about which lenders they consent to be contacted by 10.

- Competition and Innovation: The rule could intensify competition in the subprime lending market. Lenders with strong brand recognition and established customer relationships may have an advantage, while those who rely heavily on lead generation may need to adapt their strategies. This could drive innovation in customer acquisition and engagement, as lenders seek new ways to connect with borrowers and build trust.

Consumer Behavior: The rule could empower consumers to be more discerning about who they share their information with and what kind of communication they receive. This could lead to a more informed and engaged borrower base, as consumers become more active participants in the lending process.

Conclusion

The FCC’s decision to postpone the one-to-one consent rule provides subprime lenders with a critical window of opportunity. Lenders should use this time to proactively prepare for the eventual implementation of the rule by:

- Reviewing and updating consent forms and procedures: Ensure that all consent forms and processes comply with the one-to-one consent requirement.

- Investing in technology and training: Implement systems for obtaining, storing, and managing consent records, and train staff on the new requirements.

- Strengthening brand reputation and customer relationships: Focus on building trust and loyalty with existing customers and developing new strategies for attracting borrowers in a more consent-driven environment.

- Exploring alternative marketing channels: Diversify marketing efforts beyond telemarketing and lead generation, exploring channels like online advertising, content marketing, and partnerships.

- Monitoring industry developments and best practices: Stay informed about any further guidance or clarification from the FCC and adopt best practices for compliance and consumer protection.

Questions? Need help? Introductions?

Reach out to Jer at : Jer@theBusinessOfLending.com

4-WAYS I CAN HELP YOU!

Grab a copy of our “bible:” Learn More

Brainstorm: Learn More

The Business of Lending: Learn More

Free Bi-Monthly Newsletter: Learn More

Place your Money Lending Store on your borrower’s phone. Learn More