Enough said! I’m annoyed 😠 To Critics of Subprime loans and their APRs - Let’s Ground this Debate in Reality.

Why Legislators Are Wrong About Subprime Lending—and How It Affects You

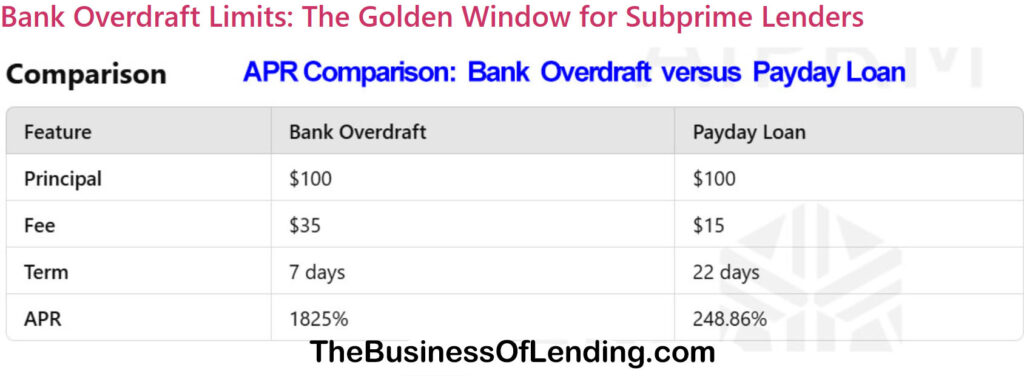

Cost vs. Alternatives: As the table below shows, a $100 payday loan with a $15 fee over 22 days results in an APR of 248.86%. Critics fixate on this figure without acknowledging that the typical bank overdraft fee for the same $100 borrowed is $35, with a mind-boggling APR of 1825%. Which is more reasonable?

Misguided Caps Harm Consumers: In states like Illinois, where arbitrary 36% APR caps were imposed, loans to subprime borrowers plummeted by 44%, leaving consumers with fewer options and pushing them toward costlier or illegal alternatives

Economic Reality of Subprime Lending: Small-dollar loans carry high fixed costs, including compliance, underwriting, and default risk. Legislators in 1916 found that small-dollar loans required rates equivalent to 108% APR today to sustain a legal market . At 36%, loans simply vanish—creating “credit deserts” that harm those the laws intend to protect.

Bankruptcy & Financial Stress: With 60% of U.S. adults living paycheck to paycheck , what critics call “predatory” loans often prevent greater financial catastrophes, like bounced checks, utility shutoffs, or repossessions. This service is about meeting urgent needs that other lenders refuse to address.

Consumer Choice: Instead of paternalistic caps, empower consumers to choose what’s right for them. Millions willingly pay for speed, convenience, and dignity over rigid bank processes and hidden fees.

Continue reading below ⬇️👇our Sponsor

Get found on your customer’s phone!

Get chosen!

Fund more loans.

Free via your Google Business Profile! > 36% APR loan products NOT a PROBLEM!

Conclusion:

A Path Forward for Empowering Subprime Consumers

This debate is not just about interest rates or loan structures—it’s about creating financial lifelines for millions of Americans who face unexpected emergencies.

The opportunity here is immense: to combine innovation, transparency, and consumer empowerment to redefine short-term lending as a force for good.

Instead of fixating on APRs as an isolated metric, let’s focus on expanding responsible access to credit. By embracing digital platforms, refining underwriting models, and tailoring solutions to consumer needs, we can meet people where they are with dignity and respect.

Policymakers, lenders, and industry advocates must work together to balance regulation with market realities, ensuring safe, affordable products remain available.

This is a moment for bold leadership.

As demand for short-term credit continues to grow, lenders with foresight can rise above misconceptions, champion consumer education, and lead the charge in building a financially inclusive future.

Let’s shift the narrative from criticism to collaboration—because when we empower consumers with the tools and options they need, we all succeed.

The way forward is clear: Innovate. Educate. Advocate. The future of lending is brighter than ever—let’s seize it together.

If my tips, tactics, strategies... saved your butt and boosted your bottom lime, how about a coffee to keep the insights brewing? Cheers to Smart Lending to the Masses

4-WAYS I CAN HELP YOU!

Grab a copy of our “bible:” Learn More

Brainstorm: Learn More

The Business of Lending: Learn More

Free Bi-Monthly Newsletter: Learn More

Google Local. Your business on your borrower’s phone. Learn More